Ethan Mitchell

A quantitative developer publishing articles about mathematics and programming.

Statistics behind finding desired cards in TCG booster packs

This article introduces the statistics behind opening trading card booster packs, answering the critical question:

how likely am I to get at least one of the cards I want? It also includes an interactive JavaScript calculator

for computing these likelihoods.

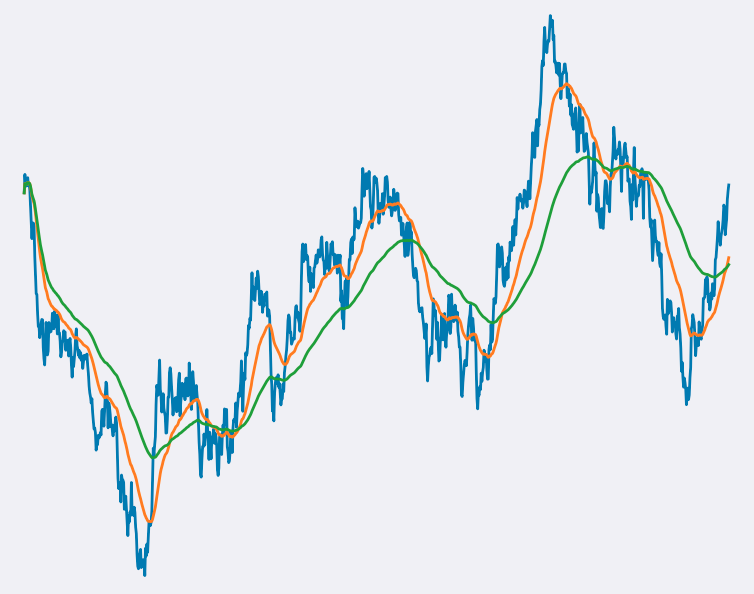

Single-pass, exponentially decayed sum and mean in Python

Given a vector of timestamped observations of a process or signal, this article derives single-pass algorithms

to compute the exponentially weighted moving sum (EWMS) and average (EWMA) and implements them in Python using

NumPy and Numba.

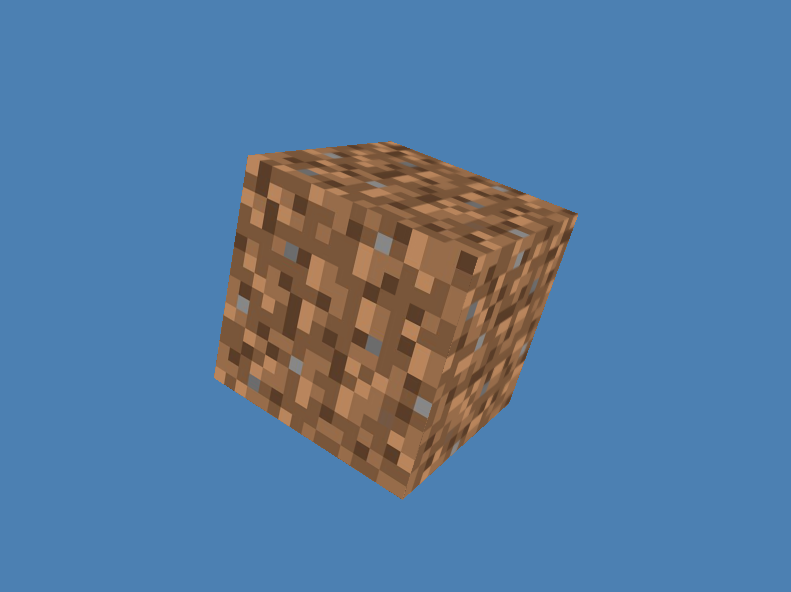

Rotating cube from scratch with PyOpenGL

This article explains the mathematics behind 3D graphics and presents a tutorial on rendering

a cube in Python using PyOpenGL.

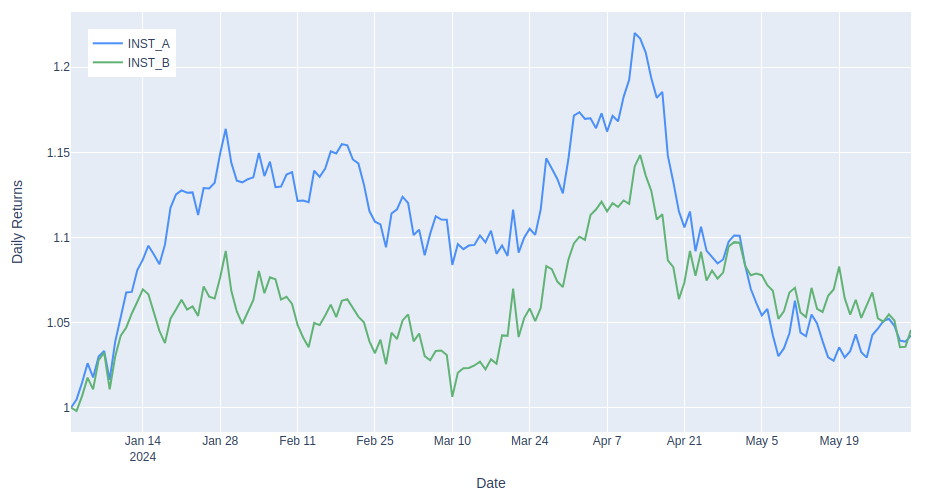

Single-pass, exponentially decayed covariance in Python

Given vectors of timestamped observations of two jointly distributed random variables, this article

derives & discusses the Python implementation of a single-pass algorithm to compute an exponentially

decayed covariance of these observations.